GG Shot – Decoded: Multi-Strategy Trading Indicator with ATR and Ichimoku

January 24, 2025 | by admin

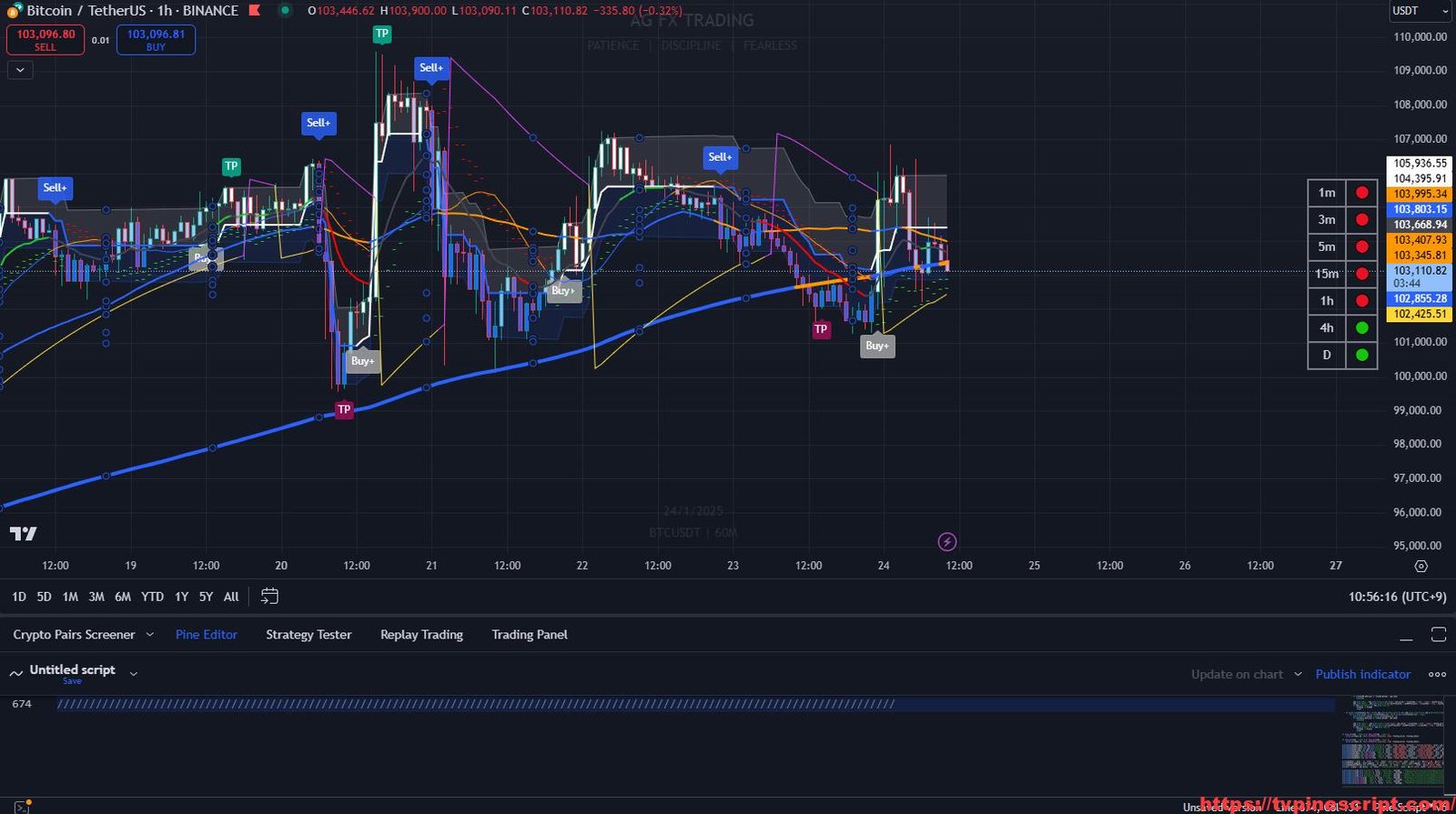

Achieving consistent profitability in trading requires the right combination of indicators that align with market conditions. The GG Shot – Decoded script is a multi-faceted trading tool that integrates ATR (Average True Range), Ichimoku Cloud, and Stop Loss strategies to provide traders with robust market insights.

This script is designed to assist traders in identifying trend direction, entry/exit points, and risk management, making it ideal for both novice and experienced traders alike.

⚠ Disclaimer: No indicator guarantees profits. The GG Shot – Decoded should be used as a reference tool alongside proper risk management and sound trading strategies.

🛠 Key Features of the GG Shot – Decoded Indicator

- ATR-Based Stop Loss Strategy:

- Automatically calculates stop-loss levels based on ATR values.

- Provides dynamic long and short stop levels to adjust for market volatility.

- Ichimoku Cloud Integration:

- Uses conversion line, base line, and lagging span for trend confirmation.

- Identifies bullish/bearish Kumo cloud zones for potential breakout opportunities.

- Trend Direction Detection:

- Built-in logic to track trend direction using price movements relative to ATR stops.

- Color-coded trend signals for quick visual identification of bullish or bearish trends.

- Pyramiding Support:

- Allows multiple positions to be opened under controlled conditions.

- Three separate pyramiding strategies to scale in or out of trades.

- Take Profit and Stop Loss Alerts:

- Customizable take-profit and stop-loss settings with visual chart alerts.

- Provides multi-level profit targets for effective risk-reward management.

- Multi-Timeframe Compatibility:

- Works effectively across various timeframes from 1-minute scalping to daily swing trading.

- Recommended for 5-minute, 15-minute, and 1-hour charts.

- Customizable Inputs for Fine-Tuning:

- Period length, multipliers, and displacement can be adjusted to match different trading styles.

- Dynamic Support/Resistance Zones:

- Tracks high/low price pivots to define areas of market reaction.

- Helps traders in setting entry/exit zones based on historical price data.

- Real-Time Buy/Sell Alerts:

- Triggers alerts when specific trade conditions are met, keeping traders informed of potential opportunities.

📊 Recommended Usage

- Scalping:

- Recommended timeframes: 1-minute to 5-minute charts.

- Use ATR-based stops for quick entries and exits.

- Day Trading:

- Best suited for 15-minute to 1-hour charts.

- Combine trend direction signals with Ichimoku cloud analysis.

- Swing Trading:

- Optimal for 4-hour to daily charts.

- Use multi-level take profits and pyramiding for long-term trend positions.

🔍 Script Evaluation

- Functionality: 4.7/5

A well-rounded script that integrates multiple trading strategies effectively. - Ease of Use: 4.0/5

Might require a learning curve for beginners due to the complexity of settings. - Accuracy: 4.6/5

Reliable in trending markets but may generate false signals in ranging conditions if used without confirmation. - Repainting Analysis:

The script does not repaint. Signals are based on confirmed price levels, making it suitable for live trading and backtesting. - Optimal Timeframes:

- Scalping: 1-minute to 5-minute charts.

- Day Trading: 15-minute to 1-hour charts.

- Swing Trading: 4-hour to daily charts.

- Overall Score: 4.5/5

A powerful script for traders seeking an automated yet flexible trading approach.

//@version=5

indicator('GG Shot - Decoded', overlay=true)

length = input(title='Period', defval=1)

mult = input.float(title='Multiplier', step=0.1, defval=13)

//ichimoku inputs

conversionPeriods = input.int(9, minval=1, title='Conversion Line Periods')

basePeriods = input.int(26, minval=1, title='Base Line Periods')

laggingSpan2Periods = input.int(52, minval=1, title='Lagging Span 2 Periods')

displacement = input.int(26, minval=1, title='Displacement')

//algo

atr = mult * ta.atr(length)

//kumo

donchian(len) =>

math.avg(ta.lowest(len), ta.highest(len))

conversionLine = donchian(conversionPeriods)

baseLine = donchian(basePeriods)

leadLine1 = math.avg(conversionLine, baseLine)

leadLine2 = donchian(laggingSpan2Periods)

longStop = hl2 - atr

longStopPrev = nz(longStop[1], longStop)

longStop := close[1] > longStopPrev ? math.max(longStop, longStopPrev) : longStop

shortStop = hl2 + atr

shortStopPrev = nz(shortStop[1], shortStop)

shortStop := close[1] < shortStopPrev ? math.min(shortStop, shortStopPrev) : shortStop

dir = 1

dir := nz(dir[1], dir)

dir := dir == -1 and close > shortStopPrev ? 1 : dir == 1 and close < longStopPrev ? -1 : dir

longColor = color.blue

shortColor = color.blue

////////////////////////////////////////////////////////////

// Conditions 1

longCond = bool(na)

shortCond = bool(na)

longCond := ta.crossover(close[1], shortStopPrev)

shortCond := ta.crossunder(close[1], longStopPrev)

// Conditions 2

longCond2 = bool(na)

shortCond2 = bool(na)

longCond2 := ta.crossover(close[1], shortStopPrev)

shortCond2 := ta.crossunder(close[1], longStopPrev)

// Conditions 3

longCond3 = bool(na)

shortCond3 = bool(na)

longCond3 := ta.crossover(close[1], shortStopPrev)

shortCond3 := ta.crossunder(close[1], longStopPrev)

////////////////////////////////////////////////////////////

// Count your long short conditions for more control with Pyramiding

sectionLongs = 0

sectionLongs := nz(sectionLongs[1])

sectionShorts = 0

sectionShorts := nz(sectionShorts[1])

if longCond

sectionLongs += 1

sectionShorts := 0

sectionShorts

if shortCond

sectionLongs := 0

sectionShorts += 1

sectionShorts

// Count your long short conditions for more control with Pyramiding 2

sectionLongs2 = 0

sectionLongs2 := nz(sectionLongs2[1])

sectionShorts2 = 0

sectionShorts2 := nz(sectionShorts2[1])

if longCond2

sectionLongs2 += 1

sectionShorts2 := 0

sectionShorts2

if shortCond2

sectionLongs2 := 0

sectionShorts2 += 1

sectionShorts2

// Count your long short conditions for more control with Pyramiding 3

sectionLongs3 = 0

sectionLongs3 := nz(sectionLongs3[1])

sectionShorts3 = 0

sectionShorts3 := nz(sectionShorts3[1])

if longCond3

sectionLongs3 += 1

sectionShorts3 := 0

sectionShorts3

if shortCond3

sectionLongs3 := 0

sectionShorts3 += 1

sectionShorts3

////////////////////////////////////////////////////////////

// Pyramiding

pyrl = 1

// Pyramiding 2

pyr2 = 1

// Pyramiding 3

pyr3 = 1

////////////////////////////////////////////////////////////

// These check to see your signal and cross references it against the pyramiding settings above

longCondition = longCond and sectionLongs <= pyrl

shortCondition = shortCond and sectionShorts <= pyrl

// These check to see your signal and cross references it against the pyramiding settings above 2

longCondition2 = longCond2 and sectionLongs2 <= pyr2

shortCondition2 = shortCond2 and sectionShorts2 <= pyr2

// These check to see your signal and cross references it against the pyramiding settings above 3

longCondition3 = longCond3 and sectionLongs3 <= pyr3

shortCondition3 = shortCond3 and sectionShorts3 <= pyr3

////////////////////////////////////////////////////////////

// Get the price of the last opened long or short

last_open_longCondition = float(na)

last_open_shortCondition = float(na)

last_open_longCondition := longCondition ? open : nz(last_open_longCondition[1])

last_open_shortCondition := shortCondition ? open : nz(last_open_shortCondition[1])

// Get the price of the last opened long or short 2

last_open_longCondition2 = float(na)

last_open_shortCondition2 = float(na)

last_open_longCondition2 := longCondition2 ? open : nz(last_open_longCondition2[1])

last_open_shortCondition2 := shortCondition2 ? open : nz(last_open_shortCondition2[1])

// Get the price of the last opened long or short 3

last_open_longCondition3 = float(na)

last_open_shortCondition3 = float(na)

last_open_longCondition3 := longCondition3 ? open : nz(last_open_longCondition3[1])

last_open_shortCondition3 := shortCondition3 ? open : nz(last_open_shortCondition3[1])

////////////////////////////////////////////////////////////

// Check if your last postion was a long or a short

last_longCondition = float(na)

last_shortCondition = float(na)

last_longCondition := longCondition ? time : nz(last_longCondition[1])

last_shortCondition := shortCondition ? time : nz(last_shortCondition[1])

in_longCondition = last_longCondition > last_shortCondition

in_shortCondition = last_shortCondition > last_longCondition

// Check if your last postion was a long or a short 2

last_longCondition2 = float(na)

last_shortCondition2 = float(na)

last_longCondition2 := longCondition2 ? time : nz(last_longCondition2[1])

last_shortCondition2 := shortCondition2 ? time : nz(last_shortCondition2[1])

in_longCondition2 = last_longCondition2 > last_shortCondition2

in_shortCondition2 = last_shortCondition2 > last_longCondition2

// Check if your last postion was a long or a short 3

last_longCondition3 = float(na)

last_shortCondition3 = float(na)

last_longCondition3 := longCondition3 ? time : nz(last_longCondition3[1])

last_shortCondition3 := shortCondition3 ? time : nz(last_shortCondition3[1])

in_longCondition3 = last_longCondition3 > last_shortCondition3

in_shortCondition3 = last_shortCondition3 > last_longCondition3

////////////////////////////////////////////////////////////

// Take profit

isTPl = input(true, 'Take Profit Long')

isTPs = input(true, 'Take Profit Short')

tp = input(2, 'Take Profit %')

long_tp = isTPl and ta.crossover(high, (1 + tp / 100) * last_open_longCondition) and longCondition == 0 and in_longCondition == 1

short_tp = isTPs and ta.crossunder(low, (1 - tp / 100) * last_open_shortCondition) and shortCondition == 0 and in_shortCondition == 1

// Take profit 2

isTP2 = input(true, 'Take Profit Long 2')

isTPs2 = input(true, 'Take Profit Short 2')

tp2 = input(4.5, 'Take Profit 2 %')

long_tp2 = isTP2 and ta.crossover(high, (1 + tp2 / 100) * last_open_longCondition2) and longCondition2 == 0 and in_longCondition2 == 1

short_tp2 = isTPs2 and ta.crossunder(low, (1 - tp2 / 100) * last_open_shortCondition2) and shortCondition2 == 0 and in_shortCondition2 == 1

// Take profit 3

isTP3 = input(true, 'Take Profit Long 3')

isTPs3 = input(true, 'Take Profit Short 3')

tp3 = input.float(7, 'Take Profit %')

long_tp3 = isTP3 and ta.crossover(high, (1 + tp3 / 100) * last_open_longCondition) and longCondition == 0 and in_longCondition == 1

short_tp3 = isTPs3 and ta.crossunder(low, (1 - tp3 / 100) * last_open_shortCondition) and shortCondition == 0 and in_shortCondition == 1

////////////////////////////////////////////////////////////

// Stop Loss

isSLl = input(false, 'Stop Loss Long')

isSLs = input(false, 'Stop Loss Short')

sl = 0.0

sl := input.float(3, 'Stop Loss %')

long_sl = isSLl and ta.crossunder(low, (1 - sl / 100) * last_open_longCondition) and longCondition == 0 and in_longCondition == 1

short_sl = isSLs and ta.crossover(high, (1 + sl / 100) * last_open_shortCondition) and shortCondition == 0 and in_shortCondition == 1

// Stop Loss 2

isSLl2 = input(false, 'Stop Loss Long 2')

isSLs2 = input(false, 'Stop Loss short 2')

sl2 = 0.0

sl2 := input.float(3, 'Stop Loss %')

long_sl2 = isSLl2 and ta.crossunder(low, (1 - sl2 / 100) * last_open_longCondition2) and longCondition2 == 0 and in_longCondition2 == 1

short_sl2 = isSLs2 and ta.crossover(high, (1 + sl2 / 100) * last_open_shortCondition2) and shortCondition2 == 0 and in_shortCondition2 == 1

////////////////////////////////////////////////////////////

// Create a single close for all the different closing conditions.

long_close = long_tp or long_sl ? 1 : 0

short_close = short_tp or short_sl ? 1 : 0

// Create a single close for all the different closing conditions 2

long_close2 = long_tp2 or long_sl2 ? 1 : 0

short_close2 = short_tp2 or short_sl2 ? 1 : 0

// Create a single close for all the different closing conditions. 3

long_close3 = long_tp3 ? 1 : 0

short_close3 = short_tp3 ? 1 : 0

////////////////////////////////////////////////////////////

// Get the time of the last close

last_long_close = float(na)

last_short_close = float(na)

last_long_close := long_close ? time : nz(last_long_close[1])

last_short_close := short_close ? time : nz(last_short_close[1])

// Get the time of the last close 2

last_long_close2 = float(na)

last_short_close2 = float(na)

last_long_close2 := long_close2 ? time : nz(last_long_close2[1])

last_short_close2 := short_close2 ? time : nz(last_short_close2[1])

// Get the time of the last close 3

last_long_close3 = float(na)

last_short_close3 = float(na)

last_long_close3 := long_close3 ? time : nz(last_long_close3[1])

last_short_close3 := short_close3 ? time : nz(last_short_close3[1])

////////////////////////////////////////////////////////////

//Signals

bton(b) =>

b ? 1 : 0

//

plotchar(long_tp and last_longCondition > nz(last_long_close[1]), text='TP1', title='Take Profit Long', size=size.tiny, location=location.abovebar, color=color.new(color.green, 0))

plotchar(long_tp2 and last_longCondition2 > nz(last_long_close2[1]), text='TP2', title='Take Profit Long 2', size=size.tiny, location=location.abovebar, color=color.new(color.green, 0))

//

plotchar(short_tp and last_shortCondition > nz(last_short_close[1]), text='TP1', title='Take Profit Short', size=size.tiny, location=location.belowbar, color=color.new(color.red, 0))

plotchar(short_tp2 and last_shortCondition2 > nz(last_short_close2[1]), text='TP2', title='Take Profit Short 2', size=size.tiny, location=location.belowbar, color=color.new(color.red, 0))

//

plotchar(long_tp3 and last_longCondition3 > nz(last_long_close3[1]), text='TP3', title='Take Profit Long', size=size.tiny, location=location.abovebar, color=color.new(color.green, 0))

plotchar(short_tp3 and last_shortCondition3 > nz(last_short_close3[1]), text='TP3', title='Take Profit Short', size=size.tiny, location=location.belowbar, color=color.new(color.red, 0))

//

ltp = long_tp and last_longCondition > nz(last_long_close[1]) ? (1 + tp / 100) * last_open_longCondition : na

plot(ltp, color=color.new(color.green, 100), trackprice=true, style=plot.style_linebr, linewidth=2 , title = "Take profit - 1")

//stp = short_tp and last_shortCondition > nz(last_short_close[1]) ? (1 - tp / 100) * last_open_shortCondition : na

//plot(stp, style=plot.style_linebr, trackprice=true, linewidth=3, color=color.new(color.white, 0))

//

ltp2 = long_tp2 and last_longCondition2 > nz(last_long_close2[1]) ? (1 + tp2 / 100) * last_open_longCondition2 : na

plot(ltp2, color=color.new(color.green, 100), trackprice=true, style=plot.style_linebr, linewidth=2, title = "Take profit - 2")

//stp2 = short_tp2 and last_shortCondition2 > nz(last_short_close2[1]) ? (1 - tp2 / 100) * last_open_shortCondition2 : na

//plot(stp2, style=plot.style_linebr, trackprice=true, linewidth=3, color=color.new(color.white, 0))

//

ltp3 = long_tp3 and last_longCondition3 > nz(last_long_close3[1]) ? (1 + tp3 / 100) * last_open_longCondition3 : na

plot(ltp3, color=color.new(color.green, 100), trackprice=true, style=plot.style_linebr, linewidth=2, title = "Take profit - 3")

//stp3 = short_tp3 and last_shortCondition3 > nz(last_short_close3[1]) ? (1 - tp3 / 100) * last_open_shortCondition3 : na

//plot(stp3, style=plot.style_linebr, trackprice=true, linewidth=3, color=color.new(color.white, 0))

//

//Stoploss 1 plotchar

plotchar(long_sl and last_longCondition > nz(last_long_close[1]), char='⛔', text='SL1 LONG', title='Stop Loss Long', size=size.tiny, location=location.abovebar, color=color.new(color.red, 0))

plotchar(short_sl and last_shortCondition > nz(last_short_close[1]), char='⛔', text='SL1 SHORT', title='Stop Loss Short', size=size.tiny, location=location.belowbar, color=color.new(color.red, 0))

//lsl = long_sl and last_longCondition > nz(last_long_close[1]) ? (1 - sl / 100) * last_open_longCondition : na

//plot(lsl, style=plot.style_linebr, linewidth=3, color=color.new(color.white, 0))

//ssl = short_sl and last_shortCondition > nz(last_short_close[1]) ? (1 + sl / 100) * last_open_shortCondition : na

//plot(ssl, style=plot.style_linebr, linewidth=3, color=color.new(color.white, 0))

//Stoploss 2 plotchar

plotchar(long_sl2 and last_longCondition2 > nz(last_long_close2[1]), char='⛔', text='SL2 LONG', title='Stop Loss Long 2', size=size.tiny, location=location.abovebar, color=color.new(color.red, 0))

plotchar(short_sl2 and last_shortCondition2 > nz(last_short_close2[1]), char='⛔', text='SL2 SHORT', title='Stop Loss Short 2', size=size.tiny, location=location.belowbar, color=color.new(color.red, 0))

lsl2 = long_sl2 and last_longCondition2 > nz(last_long_close2[1]) ? (1 - sl2 / 100) * last_open_longCondition2 : na

//plot(lsl2, style=plot.style_linebr, linewidth=3, color=color.new(color.white, 0))

//ssl2 = short_sl2 and last_shortCondition2 > nz(last_short_close2[1]) ? (1 + sl2 / 100) * last_open_shortCondition2 : na

//plot(ssl2, style=plot.style_linebr, linewidth=3, color=color.new(color.white, 0))

//plot for trend

//plot(dir == 1 ? longStop : na, title="BuyLine", style=linebr, linewidth=2, color=longColor)

plotshape(dir == 1 and dir[1] == -1 ? longStop : na, title='LONG', style=shape.triangleup, location=location.belowbar, size=size.small, text='LONG', textcolor=color.new(color.green, 0), color=color.new(color.green, 0))

//plot(dir == 1 ? na : shortStop, title="SellLine", style=linebr, linewidth=2, color=shortColor)

plotshape(dir == -1 and dir[1] == 1 ? shortStop : na, title='SHORT', style=shape.triangledown, location=location.abovebar, size=size.small, text='SHORT', textcolor=color.new(color.red, 0), color=color.new(color.red, 0))

//kumo plots

//plot(conversionLine, color=#0496ff, title="Conversion Line")

//plot(baseLine, color=#991515, title="Base Line")

//plot(close, offset = -displacement, color=#459915, title="Lagging Span")

//K1 = plot(leadLine1, offset=displacement, color=color.new(color.green, 0), title='Lead 1')

//K2 = plot(leadLine2, offset=displacement, color=color.new(color.red, 0), title='Lead 2')

//fill(K1, K2, leadLine1 > leadLine2 ? color.green : color.red, transp=90)

//barcolor(dir == 1 ? color.green : color.red)

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Functions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Conditional Sampling EMA Function

Cond_EMA(x, cond, n) =>

var val = array.new_float(0)

var ema_val = array.new_float(1)

if cond

array.push(val, x)

if array.size(val) > 1

array.remove(val, 0)

if na(array.get(ema_val, 0))

array.fill(ema_val, array.get(val, 0))

array.set(ema_val, 0, (array.get(val, 0) - array.get(ema_val, 0)) * (2 / (n + 1)) + array.get(ema_val, 0))

EMA = array.get(ema_val, 0)

EMA

//Conditional Sampling SMA Function

Cond_SMA(x, cond, n) =>

var vals = array.new_float(0)

if cond

array.push(vals, x)

if array.size(vals) > n

array.remove(vals, 0)

SMA = array.avg(vals)

SMA

//Standard Deviation Function

Stdev(x, n) =>

math.sqrt(Cond_SMA(math.pow(x, 2), 1, n) - math.pow(Cond_SMA(x, 1, n), 2))

//Range Size Function

rng_size(x, scale, qty, n) =>

ATR = Cond_EMA(ta.tr(true), 1, n)

AC = Cond_EMA(math.abs(x - x[1]), 1, n)

SD = Stdev(x, n)

rng_size = scale == 'Pips' ? qty * 0.0001 : scale == 'Points' ? qty * syminfo.pointvalue : scale == '% of Price' ? close * qty / 100 : scale == 'ATR' ? qty * ATR : scale == 'Average Change' ? qty * AC : scale == 'Standard Deviation' ? qty * SD : scale == 'Ticks' ? qty * syminfo.mintick : qty

rng_size

//Two Type Range Filter Function

rng_filt(h, l, rng_, n, type, smooth, sn, av_rf, av_n) =>

rng_smooth = Cond_EMA(rng_, 1, sn)

r = smooth ? rng_smooth : rng_

var rfilt = array.new_float(2, (h + l) / 2)

array.set(rfilt, 1, array.get(rfilt, 0))

if type == 'Type 1'

if h - r > array.get(rfilt, 1)

array.set(rfilt, 0, h - r)

if l + r < array.get(rfilt, 1)

array.set(rfilt, 0, l + r)

if type == 'Type 2'

if h >= array.get(rfilt, 1) + r

array.set(rfilt, 0, array.get(rfilt, 1) + math.floor(math.abs(h - array.get(rfilt, 1)) / r) * r)

if l <= array.get(rfilt, 1) - r

array.set(rfilt, 0, array.get(rfilt, 1) - math.floor(math.abs(l - array.get(rfilt, 1)) / r) * r)

rng_filt1 = array.get(rfilt, 0)

hi_band1 = rng_filt1 + r

lo_band1 = rng_filt1 - r

rng_filt2 = Cond_EMA(rng_filt1, rng_filt1 != rng_filt1[1], av_n)

hi_band2 = Cond_EMA(hi_band1, rng_filt1 != rng_filt1[1], av_n)

lo_band2 = Cond_EMA(lo_band1, rng_filt1 != rng_filt1[1], av_n)

rng_filt = av_rf ? rng_filt2 : rng_filt1

hi_band = av_rf ? hi_band2 : hi_band1

lo_band = av_rf ? lo_band2 : lo_band1

[hi_band, lo_band, rng_filt]

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Inputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Filter Type

f_type = input.string(defval='Type 1', options=['Type 1', 'Type 2'], title='Filter Type')

//Movement Source

mov_src = input.string(defval='Close', options=['Wicks', 'Close'], title='Movement Source')

//Range Size Inputs

rng_qty = input.float(defval=8, minval=0.0000001, title='Range Size')

rng_scale = input.string(defval='Average Change', options=['Points', 'Pips', 'Ticks', '% of Price', 'ATR', 'Average Change', 'Standard Deviation', 'Absolute'], title='Range Scale')

//Range Period

rng_per = input.int(defval=40, minval=1, title='Range Period (for ATR, Average Change, and Standard Deviation)')

//Range Smoothing Inputs

smooth_range = input(defval=true, title='Smooth Range')

smooth_per = input.int(defval=150, minval=1, title='Smoothing Period')

//Filter Value Averaging Inputs

av_vals = input(defval=false, title='Average Filter Changes')

av_samples = input.int(defval=2, minval=1, title='Number Of Changes To Average')

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Definitions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//High And Low Values

h_val = mov_src == 'Wicks' ? high : close

l_val = mov_src == 'Wicks' ? low : close

//Range Filter Values

[h_band, l_band, filt] = rng_filt(h_val, l_val, rng_size((h_val + l_val) / 2, rng_scale, rng_qty, rng_per), rng_per, f_type, smooth_range, smooth_per, av_vals, av_samples)

//Direction Conditions

var fdir = 0.0

fdir := filt > filt[1] ? 1 : filt < filt[1] ? -1 : fdir

upward = fdir == 1 ? 1 : 0

downward = fdir == -1 ? 1 : 0

//Colors

filt_color = upward ? #05ff9b : downward ? #ff0583 : #cccccc

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Outputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Filter Plot

filt_plot = plot(filt, color=dir == 1 ? color.green : color.red, linewidth=3, title='Trend Line', transp=0)

//Alerts

alertcondition(dir == 1 and dir[1] == -1 ? longStop : na, title='Buy', message='Buy!')

alertcondition(dir == 1 and dir[1] == -1 ? longStop : na, title='Buy', message='Buy!')

alertcondition(dir == 1 and dir[1] == -1 ? longStop : na, title='Buy', message='Buy!')

alertcondition(dir == -1 and dir[1] == 1 ? shortStop : na, title='Sell', message='Sell!')

//TP1 & SL1

alertcondition(bton(long_tp and last_longCondition > nz(last_long_close[1])), title='TP1 LONG')

alertcondition(bton(short_tp and last_shortCondition > nz(last_short_close[1])), title='TP1 SHORT')

alertcondition(bton(long_sl and last_longCondition > nz(last_long_close[1])), title='SL1 LONG')

alertcondition(bton(short_sl and last_shortCondition > nz(last_short_close[1])), title='SL1 SHORT')

//TP2 & SL2

alertcondition(bton(long_tp2 and last_longCondition2 > nz(last_long_close2[1])), title='TP2 LONG')

alertcondition(bton(short_tp2 and last_shortCondition2 > nz(last_short_close2[1])), title='TP2 SHORT')

alertcondition(bton(long_sl2 and last_longCondition2 > nz(last_long_close2[1])), title='SL2 LONG')

alertcondition(bton(short_sl2 and last_shortCondition2 > nz(last_short_close2[1])), title='SL2 SHORT')

//TP3

alertcondition(bton(long_tp3 and last_longCondition3 > nz(last_long_close3[1])), title='TP3 LONG')

alertcondition(bton(short_tp3 and last_shortCondition3 > nz(last_short_close3[1])), title='TP3 SHORT')

🛠 How to Apply the GG Shot – Decoded Indicator in TradingView

- Open TradingView and log in.

- Go to the Pine Script Editor at the bottom of the screen.

- Copy and paste the provided script code.

- Click Save, then name the script (e.g., “GG Shot Decoded”).

- Click Add to Chart to visualize the indicator.

- Adjust input settings based on your trading preferences and asset type.

💡 Additional Trading Tips

- Combine with Momentum Indicators:

Use RSI or MACD alongside this script to validate buy/sell signals. - Risk Management is Key:

Adjust stop-loss levels according to market volatility to minimize losses. - Trade with the Trend:

Always trade in the direction of the identified trend for higher probability trades.

🎯 Final Thoughts

The GG Shot – Decoded indicator combines multiple trading strategies into a single comprehensive tool that can help traders capture market opportunities with precision. Whether you’re looking to scalp quick profits or hold positions for long-term gains, this script offers the flexibility and reliability needed for informed decision-making.

However, remember that no trading tool is foolproof, and using this indicator in combination with market analysis and risk management will lead to better results.

Stay ahead of the market with GG Shot – Decoded and elevate your trading game today! 🚀

RELATED POSTS

View all

TradeWortex Indicator: A Multi-Faceted Trading Tool for Trend and Volatility Analysis

January 21, 2025 | by admin

Frost Algo Version 3.0 – R-Engineered: Advanced Trading Insights for Modern Traders

January 3, 2025 | by admin

The REAL-GAINS Algo: A Comprehensive Range Filter Strategy for Precise Market Entries

January 24, 2025 | by admin